To convert or not?

To convert or not?

We see an increasing number of companies and founders looking to raise rounds based on convertible notes. While convertible notes are fairly common in the US for rounds preceding the Series A, non-priced rounds are catching up in India. A number of marquee VCs including Sequoia, Accel, etc. have started writing cheques for convertible rounds through their accelerator/ early-stage programs. We pen down our views on convertible vs priced rounds here:

A convertible round involves a company raising a sum of money where the valuation is deferred until the next ‘priced’ round. The rationale behind deferring the valuation is that there is no practical/ generally accepted way of valuing early-stage companies. Usually, a company offers a discount (10-25%) to the price set in the next round whilst promising to raise in a certain time frame. Early-stage investors also prefer to have a cap and a floor i.e., the maximum and minimum valuation the investor is willing to attribute to the company at this stage. However, with the rise in global liquidity, the massive potential of the Indian market, and improved exit options in Indian tech – founders are increasingly looking to raise un-priced rounds with no cap/ floor. Large VCs are also appearing to comply – Chiratae’s Sonic claims to offer a $500K cheque within a 48- hours turnaround time, Accel Atoms programme offers $250,000 as a convertible round with no cap.

The lure of a convertible round for founders is easy to see. Convertible rounds, especially the ones with no cap, offer the promise of limited/ minimal dilution for founders. Further, founders do not have to negotiate/ haggle on valuation terms with investors thereby hastening the round closure progress.

However, in our view, non-priced rounds with no caps/ floors often end up creating a misalignment between founders and investors. Let us consider three broad scenarios:

Scenario 1: Company becomes a super success and raises a priced round at a high valuation: In such a scenario, the early-stage investors will end up with a lower stake than they intended, as they are pegged to the high valuation. Thus, they are not rewarded for the value created by the company at the early stage beyond the discount!

Scenario 2: Company gains traction and raises a priced round at a reasonable valuation: In this case, the investors receive a reasonable stake and the founders too, do not suffer a heavy dilution.

Scenario 3: Company does not gain much traction and raises a priced round at a low valuation: This is where the real kicker comes in – Not only do the founders get diluted heavily in this round but also suffer from additional dilution to the discount offered in the note. Investors end up owning a significant stake in the company while founders are often shocked at the diluted shareholding they end up with. (One may argue that investors do have downside protection in a priced round – however, it is usually a weighted average conversion versus a full ratchet as is the case which will play out in the scenario)

It is pertinent to note that Scenario 2 and 3 are likely to play out in more than 8 of 10 companies. Thus, whilst investors are likely to not make a decent return in the early stage; and in the unlikely case that they do, unpriced rounds also do not allow them the benefit of the markup.

From the perspective of founders as well, most do not end up at the stake they envisioned. Convertible notes tend to get complicated in terms of how they are priced, and complexity often causes unintended consequences in subsequent rounds. Tracking dilution easily, accurately and in real-time enables founders to plan out their seed round, but also to plan for their Series A.

Unpriced rounds obfuscate the real cap table both for the investor and the founders as well! As Fred Wilson puts it, convertibles put the ‘founder in the difficult position of promising an amount of ownership to an angel/seed investor that they cannot actually deliver down the round when the notes convert’.

We also researched the advent of convertible notes in the mature Silicon Valley ecosystem:

Convertible rounds were championed in the US late in the first decade of this century. YCombinator was one of the early pioneers pushing for convertibles.

However, a look at the valuation terms over time from roughly 2010 onwards is interesting to note:

· The initial model was a 7% equity stake in exchange for a sum that depended on the number of founders—$17,000 per founder on average.

· In 2011, YCVC began to offer $150,000 to every startup selected using an uncapped convertible note. This number was eventually was brought down to $80,000 (in addition to the equity investment by Y Combinator)

· 2013 – ‘SAFEs’ introduced by YCombinator

· Iteration in 2014 - $120k for 7% on pre-money terms. The investment would come in two chunks, representing a flat 7% of the company

· 2018 - $150K investment for 7% will be made on a post-money YC Safe.

· 2020 - $125K in return for 7% of your company using a post-money YC Safe. Future pro-rata restricted to 4%

YC which originally propounded convertible rounds eventually settled on post-money-priced rounds! Even further, YC moved away from pre-money safe agreements (i.e., YC would not be diluted by option pools created by subsequent option pools created by investors). In their own words “The convertible notes and safes we used got complicated in terms of how they got priced … It was hard for founders to actually predict how much total dilution they were looking at”. “We believe the post-money safe is simpler, making ownership and dilution easier to understand…”

Thus, after over a decade, it is clear that priced rounds are more beneficial to investors & founders in the long run. To their credit, the original move of YC towards convertible rounds was driven by a need for speed and they adjusted their terms quickly to provide for the emerging consequences in future fund-raises.

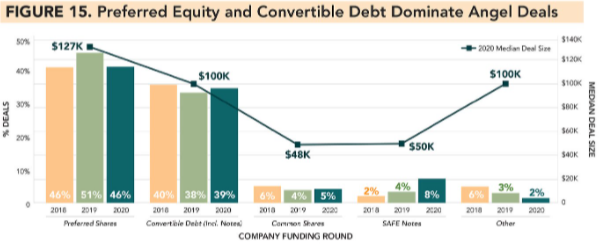

Most sophisticated investors such as micro-VCs or super angels prefer to invest via a priced round rather than a convertible note, but can often be dragged into a convertible note financing. This is also evident as per the Angels Funders Report 2021: 1 of every 2 angel deals are in the form of preferred shares – dispelling the popular notion that convertibles/ SAFEs are the norm in the US.

Source: Angels Funders Report 2021

So, does this mean that convertible and SAFE notes are not useful?

In our experience there are certainly some use-cases for convertible notes:

- Act as a bridge for the company to achieve a major milestone over a short-term

- Extension of the runway by insiders whilst planning a round

Convertibles are best used in a scenario where there is reasonable certainty of the likelihood of a priced round in the next 6 -12 months. However, to simply use them as a mechanism to postpone pricing equity until the valuation is inflated or to drag on the round until a lead investor puts in the serious dough is a red flag in our view.

We also believe that the early-stage convertible rounds offered by marquee VCs in India work for them as they are in a position to control the Series A/ B rounds. As the Ken writes about Sequoia's Surge ‘The competitive-based, self-service format of startups submitting applications is an efficient and inexpensive filter to learn about these companies…. In the worst-case scenario for Sequoia, it represents an inexpensive call option to take a punt on an entire cohort of companies.’ However, startups also need to be wary about the signalling risks that come with a large VC not participating in a Series A from startups out of its accelerator program – This is one of the major problems which YC faced as well.

At Malpani Ventures, it is our belief that the right founders will ultimately do right for the investors in the company. Whilst convertible and SAFE notes are not our preferred option, we may make calculated bets (always with a cap & floor + timeline!) to work with the founders we really like. However largely our bets shall always be in priced rounds. Do write to Siddharth or me with your views!